In this article we will discuss how to compute a variance-covariance matrix using Python.

Table of Contents

- Introduction

- Variance-covariance matrix explained

- Variance-covariance matrix example

- Create a sample DataFrame

- Compute variance-covariance matrix using Python

- Conclusion

Introduction

A variance-covariance matrix is a square matrix (has the same number of rows and columns) that gives the covariance between each pair of elements available in the data.

Covariance measures the extent to which to variables move in the same direction.

In the variance-covariance matrix, variances of variables appear on the diagonal and covariances of variables are all other elements of the matrix.

To continue following this tutorial we will need the following Python library: pandas.

If you don’t have them installed, please open “Command Prompt” (on Windows) and install them using the following code:

pip install pandas

Books I recommend:

- Python Crash Course

- Automate the Boring Stuff with Python

- Beyond the Basic Stuff with Python

- Serious Python

Variance-Covariance Matrix Explained

A covariance matrix is:

- Symmetric

The square matrix is equal to its transpose: \( A = A^T \). - Positive semi-definite

- With main diagonal containing the variances (covariances of variables on themselves)

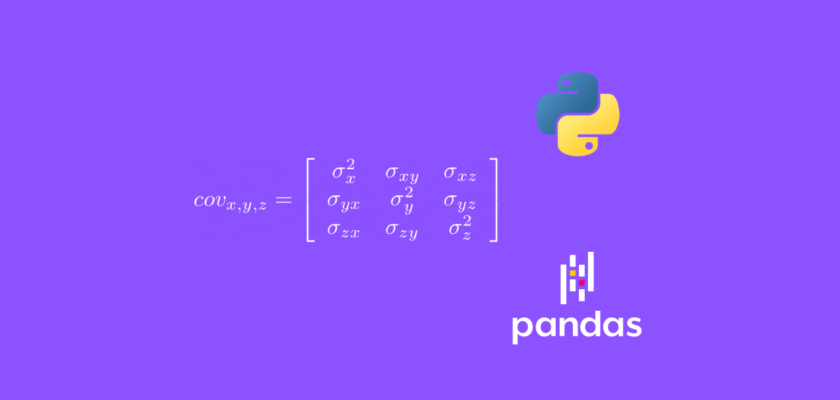

$$

cov_{x,y,z} = \left[ \begin{array}{ccc}

cov_{x,x} & cov_{x,y} & cov_{x,z} \\

cov_{y,x} & cov_{y,y} & cov_{y,z} \\

cov_{z,x} & cov_{z,y} & cov_{z,z}

\end{array} \right]

= \left[ \begin{array}{ccc}

\sigma^2_{x} & \sigma_{xy} & \sigma_{xz} \\

\sigma_{yx} & \sigma^2_{y} & \sigma_{yz} \\

\sigma_{zx} & \sigma_{zy} & \sigma^2_{z}

\end{array} \right]

$$

where each covariance can be computed by the following formula (replacing x, y, z values):

$$

cov_{x,y} = E[(X – E[X])(Y – E[Y])] = \frac{\sum(x_i – \bar{x})(y_i – \bar{y})}{N-1}

$$

Variance-Covariance Matrix Example

First, let’s consider some sample data to work with:

| Age | Experience | Salary |

| 25 | 2 | 2000 |

| 32 | 6 | 3000 |

| 37 | 9 | 3500 |

Alternatively, the above table can be represented as a matrix:

$$A = \begin{bmatrix} 25 & 2 & 2000 \\ 32 & 6 & 3000 \\ 37 & 9 & 3500 \end{bmatrix}$$

Then the covariance matrix of \(A\) will look like:

$$

cov_{a,e,s} = \left[ \begin{array}{ccc}

cov_{a,a} & cov_{a,e} & cov_{a,s} \\

cov_{e,a} & cov_{e,e} & cov_{e,s} \\

cov_{s,a} & cov_{s,e} & cov_{s,s}

\end{array} \right]

$$

where \(a\), \(e\), \(s\) are Age, Experience, and Salary respectively.

Finally, using the covariance formula:

$$

cov_{x,y} = E[(X – E[X])(Y – E[Y])] = \frac{\sum(x_i – \bar{x})(y_i – \bar{y})}{N-1}

$$

we can calculate the covariance between each pair and populate the variance-covariance matrix:

\( cov_{a,a} = \frac{\sum(Age_i – \bar{Age})(Age_i – \bar{Age})}{N-1} = \\ = \frac{(25-31.33)(25-31.33) + (32-31.33)(32-31.33) + (37-31.33)(37-31.33)}{3-1} = \\ = \frac{40.0689 + 0.4489 + 32.1489}{2} \approx 36.33 \)

\( cov_{a,e} = cov_{e,a} = \frac{\sum(Age_i – \bar{Age})(Experience_i – \bar{Experience})}{N-1} = \\

= \frac{(25-31.33)(2-5.66) + (32-31.33)(6-5.66) + (37-31.33)(9-5.66)}{3-1} = \\ = \frac{23.1678 + 0.2278 + 18.9378}{2} \approx 21.17 \)

\( cov_{a,s} = cov_{s,a} = \frac{\sum(Age_i – \bar{Age})(Salary_i – \bar{Salary})}{N-1} = \\

= \frac{(25-31.33)(2,000-2,833.33) + (32-31.33)(3,000-2,833.33) + (37-31.33)(3,500-2,833.33)}{3-1} = \\ = \frac{5,274.9789 + 111.6689 + 3,780.0189}{2} \approx 4,583.33 \)

\( cov_{e,e} = \frac{\sum(Experience_i – \bar{Experience})(Experience_i – \bar{Experience})}{N-1} = \\

= \frac{(2-5.67)(2-5.67) + (6-5.67)(6-5.67) + (9-5.67)(9-5.67)}{3-1} = \\ = \frac{13.4689 + 0.1089 + 11.0889}{2} \approx 12.33 \)

\( cov_{e,s} = cov_{s,e} = \frac{\sum(Experience_i – \bar{Experience})(Salary_i – \bar{Salary})}{N-1} = \\

= \frac{(2-5.67)(2,000-2,833.33) + (6-5.67)(3,000-2,833.33) + (9-5.67)(3,500-2,833.33)}{3-1} = \\ = \frac{3,058.3211 + 55.0011 + 2,220.0111}{2} \approx 2,666.67 \)

\( cov_{s,s} = \frac{\sum(Salary_i – \bar{Salary})(Salary_i – \bar{Salary})}{N-1} = \\

= \frac{(2,000-2,833.33)(2,000-2,833.33) + (3,000-2,833.33)(3,000-2,833.33) + (3,500-2,833.33)(3,500-2,833.33)}{3-1} = \\ = \frac{694,438.8889 + 27,778.8889 + 444,448.889}{2} \approx 583,333.33 \)

Using the calculated covariance values, we can now populate the variance-covariance matrix:

$$

cov_{a,e,s} = \left[ \begin{array}{ccc}

36.33 & 21.17 & 4,583.33 \\

21.17 & 12.33 & 2,666.67 \\

4,583.33 & 2,666.67 & 583,333.33

\end{array} \right]

$$

Create a sample DataFrame

Let’s create a sample Pandas DataFrame with three variables: Age, Experience, Salary with a few observations for each:

import pandas as pd

df = pd.DataFrame(

{'Age': [25, 32, 37],

'Experience': [2, 6, 9],

'Salary': [2000, 3000, 3500]}

)

print(df)

And we get:

Age Experience Salary

0 25 2 2000

1 32 6 3000

2 37 9 3500Compute variance-covariance matrix using Python

Using the .cov() method of the Pandas DataFrame we are are able to compute the variance-covariance matrix using Python:

cov_matrix = df.cov()

print(cov_matrix)

And we get:

Age Experience Salary

Age 36.333333 21.166667 4583.333333

Experience 21.166667 12.333333 2666.666667

Salary 4583.333333 2666.666667 583333.333333Conclusion

In this article we discussed how to compute a variance-covariance matrix using Python.

Feel free to leave comments below if you have any questions or have suggestions for some edits and check out more of my Statistics articles.